The following provides a summary of the backdating scandal and the use of forensic economics to uncover it. For a broader overview of forensic economics in academia, click here.

CEO pay

In 2020, CEOs at the largest 350 US corporations made an average of $24 million, meaning that their daily pay was about the same as the typical workers’ annual pay. You would think that CEOs and other top executives are content with their colossal pay. Well, not all of them. There is plenty of evidence that executives try to extract more pay, sometimes in sneaky ways. That is what happened on a grand scale during the 1990s and the beginning of the 2000s.

Stock option pay

A large chunk of executive pay comes in the form of stock option grants. These options give the executives the right to buy shares in their company at a pre-specified price called the exercise price. The lower the exercise price, the more valuable are the options. Importantly, the exercise price is generally set to equal the market price of the underlying stock on the grant date. That sets the stage for manipulation.

Option grant manipulation

Because the option value is higher if the exercise price is lower, executives prefer to be granted options when the stock price is at its lowest. How can they accomplish that?

- One strategy is to exploit insider information about what will happen to stock prices. If executives know that the company will soon release some good news, they should expedite the grant to occur before the news release to lock in a relatively low exercise price, a practice sometimes referred to as spring-loading. Conversely, if they know that the company will soon release some bad news, they should delay the grant to occur after the news release, a practice sometimes referred to as bullet-dodging.

- A second strategy is to manipulate the information flow to the marketplace. This might work if the grant is scheduled ahead of time to occur on a certain date and executives have discretion in the timing of news releases. For example, if an executive can choose when to release bad news, they could do it before a scheduled grant.

- A third strategy is to choose a grant date from the recent past, perhaps the last quarter or year, when the price was particularly low, a strategy referred to as backdating. To use an analogy, if the first two manipulation strategies correspond to having an information edge when betting on sports games, the third strategy is like using tomorrow’s newspaper when betting on sports games that take place today. Much easier, right?

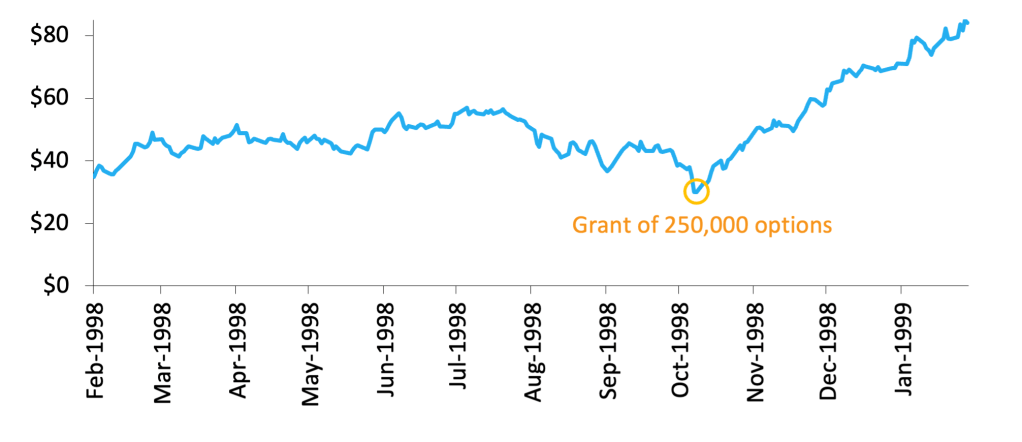

An example of backdating

In October 1998, Comverse Technology granted 250,000 options with an exercise price of $30 to its CEO, Kobi Alexander. If the options were actually granted at the end of the fiscal year when the price was $85, the benefit of backdating a few months to obtain the lower exercise price was ($85 – $30) x 250,000 options = $13,750,000.

Why not just set the exercise price lower than the market price?

- The board and executives might prefer for the additional pay from backdating to be hidden.

- Shareholder approved option plans often require that exercise prices be no less than the fair market value of the stock on the date when the grant decision is made.

- Under accounting rules, the difference in value between the market price and exercise price results in a higher reported expense that reduces reporting earnings.

- To qualify as performance-based compensation under the tax code (which gives favorable tax treatment), the exercise price cannot be less than the market price on the grant date.

Is backdating legal?

If the practice is transparent, it might be legal. But because backdating is used to deceive shareholders, bypass company rules and accounting regulation, and cheat the IRS, it is at a minimum unethical and typically illegal. The document forgery that accompanies backdating does not help.

How do we know that backdating occurred?

David Yermack of NYU was the first researcher to document peculiar stock price patterns around option grants. In an article published in 1997, he reported that stock prices tend to increase shortly after the grants. He attributed most of this pattern to executives being granted options before predicted price increases (see spring loading above).

In a study started in 2003 and published in May 2005, I found that the tendencies first documented by Yermack intensified by the end of the 1990s and the beginning of the 2000s. In fact, not only do the stock prices for this later period increase after grants, but the prices also decrease before the grants, with a sharp reversal exactly on the grant date. The pattern is so strong that there had to be more than just grants being timed before predicted stock price movements. I also found that the overall stock market performed worse than what is normal immediately before the grants and better than what is normal immediately after the grants. Unless corporate insiders can predict short-term movements in the stock market, which is highly unlikely, the evidence pointed to backdating as the culprit.

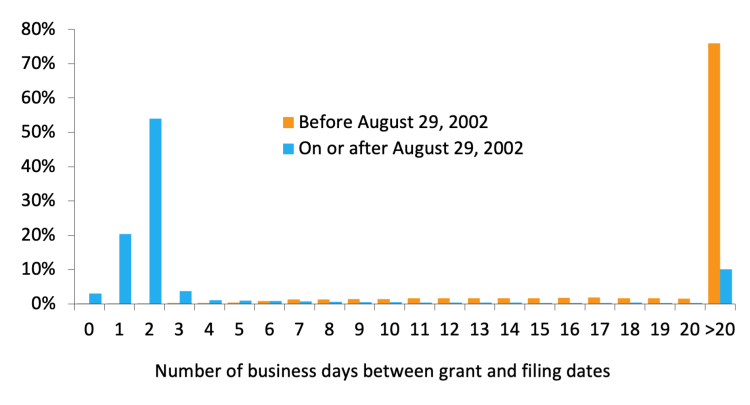

In a second study with Randy Heron of Indiana University (mostly done in 2005 and published in 2007), we examined the stock price pattern around option grants before and after a new SEC requirement in August of 2002 that option grants must be reported within two business days. The graph below shows the dramatic effect of this new requirement on the lag between the grant and filing dates.

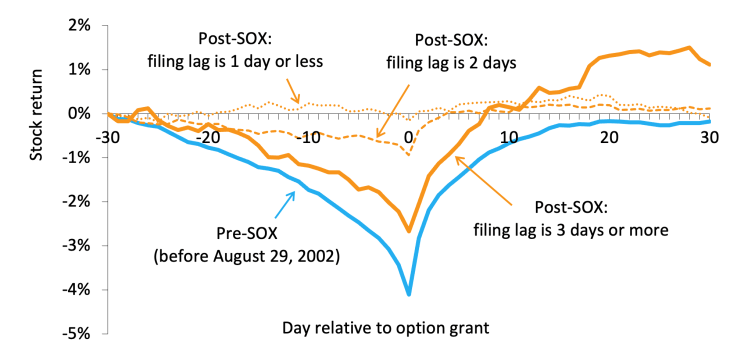

To the extent that companies complied with this new regulation, backdating should be greatly curbed. Thus, if backdating explains the stock price pattern around option grants, the price pattern should diminish following the new regulation. Indeed, we found that the stock price pattern is much weaker since the new reporting regulation took effect. Any remaining pattern is concentrated on the couple of days between the reported grant date and the filing date when backdating still might work, and for longer periods for the minority of grants that violate the two-day reporting requirements. Our evidence closed the case for backdating.

The SEC gets involved

I alerted the SEC in the spring of 2004 of my evidence of backdating and sent them some data. The SEC initiated their own confidential investigation of individual companies, though the process was slow and meticulous.

In July 2005, Silicon Valley software company Mercury Interactive Corp. announced that its board had named a special committee to investigate past stock-option grants in connection with an informal SEC probe that was initiated in November 2004. An internal investigation uncovered 49 cases in which the reported date of a Mercury stock-option grant differed from the date on which the option appears to have been actually granted. As a result, three top executives at Mercury, including the CEO, resigned in November 2005. The stock price fell 25% upon the news of the backdating instances and the executive resignations. Because the company was unable to restate the earning to account for the option backdating in a timely manner and delayed other filings of earnings with the SEC, its shares were delisted in the beginning of 2006.

The Wall Street Journal (WSJ) takes over

Prompted by the Mercury case and other SEC investigations, WSJ ran a big story on the issue of backdating on November 11, 2005. In a follow-up story, I supplied WSJ with data that helped it identify six companies as almost certain backdaters. The publication of this article on March 18, 2006, triggered chaos, resignations, and large stock price declines among the identified companies. One executive even fled the country.

A WSJ article published on May 5, 2006, summarized some of these events and the effects on shareholders’ value. For example, the article suggested that the market capitalization of the giant health insurer UnitedHealth Group dropped $13 billion (yes, that is billion with a “b”) since questions about option-granting practices surfaced.

How prevalent was backdating?

Randy Heron and I estimated that 23% of unscheduled, at-the-money grants to top executives dated between 1996 and August 2002 were backdated or otherwise manipulated. This fraction was roughly halved after the new two-day reporting requirement took effect in August 2002. We also estimated that almost 30% of firms that granted options to top executives between 1996 and 2005 manipulated one or more of these grants. This amounts to more than 2,000 firms!

The fallout

Hundreds of companies were publicly entangled in the backdating scandal. At least 70 top officials lost their jobs, and some went to prison. For example, Bill McGuire, the lauded CEO of UnitedHealth, agreed to resign and surrender more than $600 million(!) in stock option gains and retirement pay. Even Steve Jobs, who famously only received a $1 salary but massive stock option grants, admitted to being aware of backdating at Apple, and Apple promptly fired two of its lower-level executives to save upper-level executives like Jobs. Much housecleaning and litigation also occurred out of the public eye.

Yet, many firms and executives got off the hook. Backdating can be hard to prove, especially when executives tread carefully (e.g., by picking a day with a low stock price as the grant date, but not the lowest) or cover their tracks (e.g., by forging meeting minutes), and neither journalists, plaintiff lawyers, nor regulators dare to pursue fuzzy cases. Furthermore, regulators and the investment community are quite content to set precedents based on a limited set of egregious backdating cases to send a signal that backdating and similar behavior will be punished.

In July 2006, the SEC altered the reporting rules on executive compensation by, e.g., requiring disclosure of the date that the option grant decision was made. Two congressional hearings followed in September 2006, giving politicians on Capitol Hill a welcome chance to castigate greed in the executive rank.

In 2007, the WSJ was awarded the Pulitzer Prize for Public Service “for its creative and comprehensive probe into backdated stock options for business executives that triggered investigations, the ouster of top officials and widespread change in corporate America.” The Pulitzer Prize for Public Service is the only Pulitzer Prize that comes with a gold medal and is the most coveted among newspapers. It was the first time, and still the only time, that the WSJ won this prestigious award.

But when the financial crisis emerged in 2007, the attention of the media and regulators naturally shifted.